Alex Axon (Chief Experience Officer & Partner at Zitec) and Antar Turgay (Retail Banking Director at Nexent Bank) recently sat down with Wall-street.ro to discuss the strategy behind Avantaj, their award-winning app recognized at the 2026 UX Design Awards in Berlin. They noted that today’s consumers hold banking apps to the same high standards as global tech giants like Uber or Netflix.

While the interface must be as smooth as a streaming service, the stakes in banking are significantly higher. "We are dealing with people's money, which brings a different level of scrutiny and emotion," Axon explained. The core philosophy behind the app is to shield the user from technical complexity, such as compliance and backend integrations, and provide a front-end experience defined by "control and clarity".

Antar Turgay highlighted a major shift in how customers engage with credit products, especially credit cards. “Digital acceleration is no longer about simply putting card statements online; it is about redefining the entire customer experience. Today’s customers expect instant card issuance, real-time transaction visibility, seamless installment conversion, and full control directly from their mobile phones. They want to activate, block, tokenize, increase limits, or convert transactions into installments in seconds, without friction” specifies Antar Turgay.

The shift in behavior towards "mobile-first" experiences is becoming increasingly clear. Modern "mobile-first" users expect more than just digital statements; they demand a friction-free ecosystem, with intuitive client journeys, minimal documentation, and total transparency regarding balances, due dates, rewards, and benefits offered by partners. "Digitalization has significantly raised expectations. We are no longer compared only to banks, we are compared to the experience standards set by technology companies" adds the Nexent Bank representative.

The Blueprint for International Recognition

Building a banking app suited to customers’ needs is based on a strategic partnership that goes beyond simply delivering quality design or development. Axon brings up the importance of clear business goals, such as better retention, higher usage, and real differentiation in the market.

"In practice, this requires involvement from both sides. Product, IT, and marketing teams must work in an integrated manner. In banking, there are constraints related to PSD2, KYC, AML, GDPR, and integration with existing systems. If you don't deeply understand them, you risk proposing solutions that look good in a presentation but cannot be implemented," adds the Zitec representative.

In the collaboration between Zitec and Nexent Bank, the two organizations aligned from the very beginning on the overall direction, jointly assuming that customer experience is a strategic differentiator. This led to the right decisions at both product and technology level.

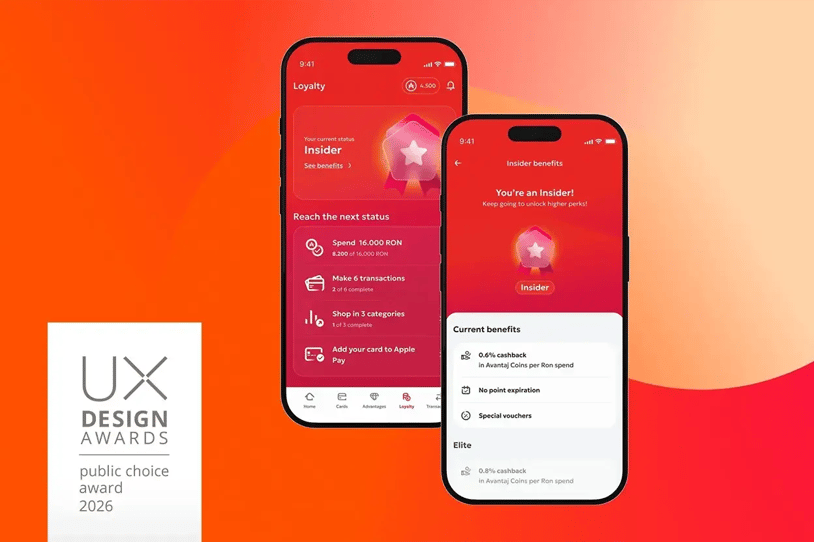

“The results of this integrated approach and our deep strategic partnership with Nexent Bank recently materialized when the Avantaj app won the Public Choice Award at the UX Design Awards 2026 in Berlin. Out of a pool of 431 participants from 46 countries, the jury selected 19 winners, and our app was recognized both by experts and the wider public for its measurable impact on user experience,” says Alex Axon.

“Our collaboration was built around a shared vision: to create a scalable, agile, credit-card-centered digital ecosystem. Technology partners today are not vendors, they are strategic co-creators. In developing the Avantaj application, we worked in agile teams that combined deep credit card expertise with technological innovation” adds Antar Turgay.

A customer journey with meaning and clarity built into every step

App users want a frictionless experience, whether for streaming or banking. In the Zitec expert's opinion, a well-built customer journey is one in which the user understands what they are doing, why they are doing it, and what they gain from it.

“Each step is clear and meaningful. In consumer lending, things become interesting when you manage to turn a financial product into an experience that creates engagement. In the Avantaj app developed with Nexent Bank, we focused on card management, virtual card generation, and especially on loyalty building” adds Alex Axon.

Features in banking apps, such as cashback or tier-based benefits, become relevant when they are easy to understand.

“The user sees progress, knows what they have gained, and returns to the app because they have a real reason to. A good customer journey means a coherent experience from the first contact with the app all the way to its recurring use,” adds the Zitec representative.

In designing the Avantaj app, Antar Turgay explains that the objective was depth, not variety. Credit cards represent an essential strategic pillar for Nexent Bank. As a result, instead of creating a generic banking app, they built a specialized digital ecosystem around this product.

“This focused approach allowed us to offer advanced card management features like providing real-time installment conversion, delivering transparent rewards tracking, integrating exclusive partner campaigns, introducing gamification and loyalty tiers. Specialization enables faster innovation and deeper engagement. Rather than being one feature among many, credit cards became the center of a curated digital experience.”

Technical Drivers of Speed and Quality

Technologies evolve rapidly, and customers expect apps to keep up with this accelerated rhythm. To keep pace with market expectations, Zitec leveraged a specific technical mix to accelerate the launch without sacrificing UX:

- Product management - understanding customer needs using accurate and complete data, and translating those needs into a set of well-prioritized features aligned with the value they bring, as well as the ability to adjust product strategy dynamically depending on market reality. At first glance this may seem like a fairly simple activity, but unfortunately we rarely see organizations in the financial industry with this role well developed, either because of a lack of data or a lack of experience in more complex digital transformation processes.

- Composable banking and distributed services - even though there are platforms that offer reasonably well-integrated products for the financial industry, they are often represented by a capable core product (such as core banking) and a series of secondary products that are very poorly developed when it comes to UX, scalability, or customization (usually mobile banking, internet banking, digital onboarding, etc.). The approach we observed to deliver much better results is composable banking, in which we mix various specialized products (especially operational processes) with custom development.

- Cloud / Software as a service - just as with product management, this is not at all a new concept, but unfortunately understanding and implementation tend to be superficial, which leads to weak results. The use of cloud platforms or software as a service tends to significantly shorten launch times, optimize costs, and greatly improve security posture, but these benefits materialize only through well-structured adoption. In our opinion, this means detailed platform technical understanding and practical testing, not just comparisons based on market share or marketing materials. Additionally, it requires technical teams specialized in cloud environments operating, by completely rethinking technical and security practices, rather than trying to transfer existing on-premises processes into the cloud.

UX, engagement and loyalty

The UX (User Experience) component directly influences product retention and usage, says Axon. In a market where most banking apps offer similar features, experience is the element that makes the difference.

“A well-built app reduces abandonment and increases loyalty. This can be seen in business indicators. In 2026, the financial institutions that treat experience as a strategic investment, rather than as a visual layer add-on, are the ones that win in the long run" adds Axon.

Asked which elements in the Avantaj application contribute most to user retention, Antar Turgay mentions the following:

- Simplicity - Easy navigation, instant card management, seamless instalment options.

- Transparency - Real-time visibility of balances, due amounts, rewards, and campaign benefits.

- Rewards - Tangible and progressive value through loyalty programs and partner ecosystems.

"Retention is not about locking customers in - it is about continuously giving them reasons to stay active.In credit cards, engagement frequency directly correlates with retention. The more relevant the experience, the stronger the relationship" specifies Antar Turgay.

The future of consumer lending

Antar believes that in the near future digital credit cards will become more personalized through the use of artificial intelligence and predictive analytics. They will be increasingly integrated into everyday ecosystems (retail, travel, e-commerce) and will offer more flexible repayment structures.

“We expect real-time credit line adjustments, predictive installment suggestions, smarter fraud prevention, greater integration with digital wallets and open banking ecosystems. The future belongs to institutions that combine financial discipline with technological agility. At Nexent Bank, we see credit cards not simply as a lending product, but as a dynamic engagement platform at the heart of the digital financial ecosystem” adds the Retail Banking Director.

We at Zitec believe that these niche digital products have matured and the growth rate will slow down. However, there are areas in the market where we believe there is significant growth potential:

- Credit cards - the market has evolved very slowly over the past 10 years due to a combination of factors. One of them was the lack of investment in building a digital ecosystem around credit cards, which were usually treated simply as a card with a few isolated merchant discounts. There is a lot of room for innovation.

- BNPL - even though there are already a few success stories in the market, we believe this product has significant potential among banks because it can help attract new customers (especially younger ones) into the banking system in a responsible way. This can help prevent those customers from having a negative first interaction with the financial industry due to the use of alternative products with excessive interest rates or lack of transparency.

Methodology

This article consolidates insights from Zitec’s CXO, Alex Axon, and Antar Turgay, Retail Banking Director at Nexent Bank, originally shared in a Wall Street Journal Romania interview on technology’s role in the financial services sector. The initial piece was produced under Zitec’s guidance in collaboration with top Romanian journalists. This derivative work offers an extended perspective and in-depth analysis of industry developments.

Share via: