Nowadays, fintechs are operating in a challenging landscape characterized by heightened competition, mounting pressures for cost efficiency and profitability, and a rapid pace of change in the industry. This environment pushes companies to prioritize streamlining operations and adopt a more strategic and pragmatic approach to implementing digital and AI initiatives.

The first step to mastering these fintech trends and challenges is knowing what they entail. So, we’ve turned to our financial technology experts to compile this master resource. Let’s dive in.

1. Adopting AI Pragmatically to Balance Investment with Impact

Source

The push to prove AI's economic efficiency begins with a broader digital transformation trend, where businesses are under pressure to better prioritize technology investments based on these initiatives' economic benefits.

Although the potential impact of AI on companies in the financial services industry is substantial, these projects are met with skepticism due to poor ROI planning and limited access to information about information security.

Still, traditional financial institutions are incumbent and slow to adapt, which poses an advantage for highly adaptive startups who know that AI is more than just a fintech trend.

Even so, the first-mover advantage had already been played. Certain fintech industry players have long decided to bet big on AI adoption, investing in research and development. As expected, some breakthroughs are starting to show, as shown by a Sailpeak report on AI’s impact on the financial industry:

- Argenta Bank reduced its annual model validation time from 3-4 months to just 2 weeks using AI-driven automation.

- Crelan uses AI to enhance its Anti-Money Laundering (AML) processes, which helps examine more transactions in less time.

- Europ Assistance automates 78% of its manual mailroom tasks within six weeks, saving 495 monthly hours and allowing staff to focus on more value-added activities. Let me know if there is anything else I can help you with.

In addition, another fintech in the BNPL sector, Klarna, reduced its workforce from 5,000 to 3,800 in the past year. What’s more, they plan to reduce it to 2,000 employees, all with the help of AI.

Despite these advancements, widespread AI adoption remains challenging, often facing issues like:

- Integration barriers

- A shortage of skilled AI professionals

- The complexity of AI systems and the need to comply with data governance rules

Source

There’s no denying the economic potential of this tech in the financial sector. As McKinsey suggests, Gen AI could boost operating profits by 9% to 15% through cost savings.

Still, AI is no one-size-fits-all solution nor a universal ROI generator. These investments come with risks, amplified by the lack of know-how behind deploying such technologies. That’s why Gartner predicts that by 2028, more than 50% of organizations invested in large AI models will abandon their initiatives.

Source

As such, will financial players take a leap of faith and strategically invest in AI while facing uncertainty, or will resistance to change persist?

Remember that, if done right, implementing AI solutions for sustainable growth is a winning approach. The key to success is first to assess the level of change that the organization is ready and willing to undergo, the technical expertise and tool stack required, and the specific AI use case the fintech industry player wants to achieve.

Partner with technology leaders to define your strategy, assess business risks, and test your digital endeavours’ viability with a tailored Proof of Concept.

2. Optimizing Costs for Long-Term Operational Efficiency

The challenge of cost optimization is, in fact, the challenge of ensuring that the approach is sustainable and aligned with long-term strategic goals. In the fintech industry and beyond, effective cost optimization goes beyond plain cost-cutting. It involves a 360 view of:

- Expenditures

- Resource optimization

- The reinvestment of savings into initiatives that drive value for the organization and its customers

For companies keen on cutting fixed and variable costs, Gartner’s cost optimization frame narrows down some interesting areas of expenditure reconfiguration:

Source

Still, we believe in cost-optimization through powerful technology investments that drive long-term value, rather than plain expenditure adjustments.

|

Consider Pegasus Legal Capital, a firm blending financial services with legal expertise. As it expanded, Pegasus faced a considerable issue—its outdated CRM system couldn’t keep up with the influx of leads and contract management duties. By partnering with Zitec, the company switched to its freshly built Orion platform, which automates lead intake, contract generation, and digital signatures. The result? 👇 Pegasus saw contract generation time cut by over 30 times while digital signing rates soared from under 10% to over 50%. |

3. Enhancing Customer Acquisition and Maximizing Lifetime Value

In a business environment where onboarding new customers costs 5x more than retaining existing ones, all while traditional advertising budgets are shrinking, targeting the right customers has become key.

Fintech companies must focus on identifying high-value profiles that generate the most revenue. Then, they need to optimize acquisition efforts around these high-value customers. To achieve this, the focus should fall on making strategic marketing decisions, such as:

- Boosting customer engagement based on data through personalized cross-selling and up-selling opportunities. For example, offering tailored loan consolidation options or increased transaction limits can improve customer satisfaction and loyalty.

- Engaging current customers through better user experiences, frictionless processes, and new features. With most businesses prioritizing customer acquisition over retention, keeping customers satisfied is necessary for long-term success.

The challenge? Mastering customer operations requires a strategic approach to data governance and customer engagement — all of which require the talent and expertise typically found in enterprise-level institutions, rather than smaller fintech industry players.

But what if enterprise-grade-level teams and top-level tech stacks were at your fingertips?With Zitec, that’s possible. Reach out today.

|

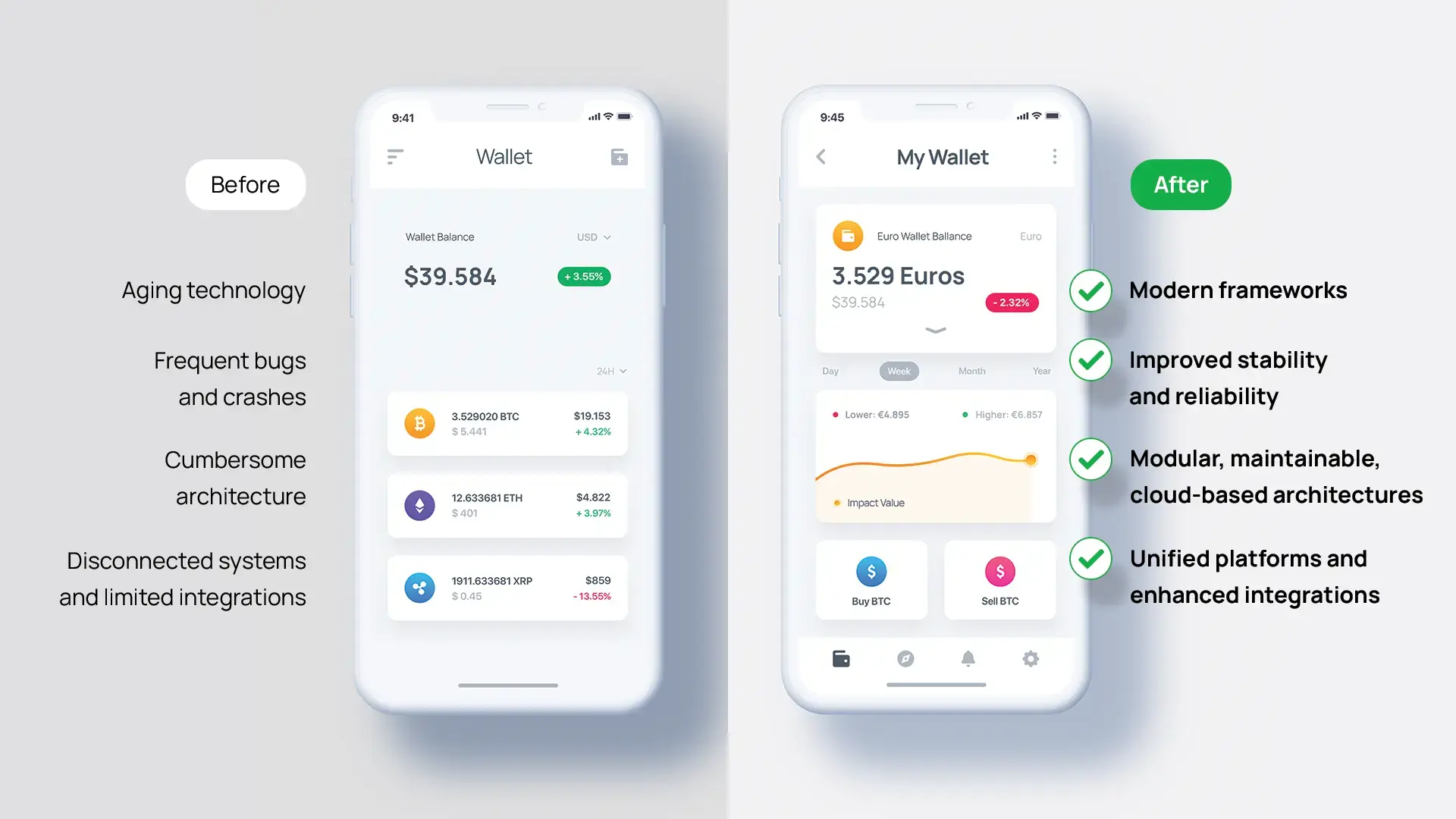

4. Building Scalable and Resilient Business Models in High-Demand Environments

As fintechs grow, they must handle growing volumes of transactions while ensuring little to no downtime against all potential failures. The stakes are high: downtime or performance lag can lead to financial losses, erode customer trust, and trigger regulatory scrutiny.

As fintechs grow, they must handle growing volumes of transactions while ensuring little to no downtime against all potential failures. The stakes are high: downtime or performance lag can lead to financial losses, erode customer trust, and trigger regulatory scrutiny.

The challenge is particularly high in the financial sector, where real-time processing and high availability are crucial. How so? Let us exemplify this fintech challenge for more clarity:

- A neobank that experiences downtime could face high customer churn

- A payment gateway's inability to scale during peak demand periods might result in failed transactions and lost revenue.

Looking ahead, the ability to scale efficiently while maintaining resilience will be a real differentiator in the financial space.

The key? Fintechs must invest in cloud architectures, such as:

- Distributed systems (so if one component fails, others can take over to minimize downtime and disruptions. They are fundamental in cloud architectures to ensure high availability and resilience. Redundancy and failover capabilities can prevent single points of failure)

- Automated failover mechanisms (which automatically switch operations to a backup system without manual intervention for business continuity. These ensure business continuity during hardware failures, network issues, or disruptions. Public Cloud providers like Azure, Google, and AWS offer built-in failure protections, but the correct cloud-native setup is key to leveraging these. Combined with proper alerting and continuous DevOps & Security improvements, this ensures higher availability)

- Scalable cloud infrastructure (to remain responsive during peak times without over-provisioning during quieter periods. Auto-scaling capabilities allow fintechs to adjust resources based on demand to maintain performance during high-traffic events.)

The challenge of migrating to the cloud for financial institutions

Migrating to the cloud is a tough challenge for financial institutions due to the mix of old legacy systems, modern technologies, and strict regulatory rules they must follow. Traditional banks have heavily invested in on-premises setups, making the shift to the cloud expensive and risky. A mistake during this transition could have serious consequences.

So far, only 13% of banks have moved a large part of their IT to the cloud, but over half plan to do so by 2027 to fully maximize the benefits of cloud technology.

|

Consider one of Zitec's clients, a financial services company based in Los Angeles. The company needed to streamline and scale its operations to manage thousands of transactions daily. By partnering with Zitec, they developed a personalized ERP platform hosted entirely on Microsoft Azure and a slack bot that helped them triple their business size while only slightly increasing its underwriter team. The ERP solution eliminated the need for manual processes, reducing errors and saving time |

5. Leveraging Open Financial Data for Added Business Value Amid Regulatory Pressures

Open financial data offers the opportunity to create more personalized services and tap into new revenue streams. However, many financial institutions struggle to take advantage of this due to a lack of hands-on knowledge and expertise.

More than using the right technology, managing open data implies a shift in mindset towards making data-driven decisions. But the main issues behind this fintech challenge involve a series of interconnected factors, like:

- Complexity of data management. Open financial data is sourced from various channels, including third-party providers, government databases, and customer transactions. integrating and analyzing this data involves using advanced technologies (e.g., data analytics, machine learning) and skills many fintechs lack.

- Regulatory compliance. In the fintech industry, regulations such as GDPR and directives like PSD2 and the anticipated PSD3 add layers of difficulty. Therefore, data usage must align with legal standards while remaining practical for business operations, as non-compliance can lead to penalties and reputational damage.

- Security and privacy concerns. The open nature of financial data increases the risk of breaches and unauthorized access. Balancing risk management with the agility to leverage data is a significant challenge. Yet, the potential benefits—such as improved pricing strategies, enhanced risk management, and better customer experiences—are substantial.

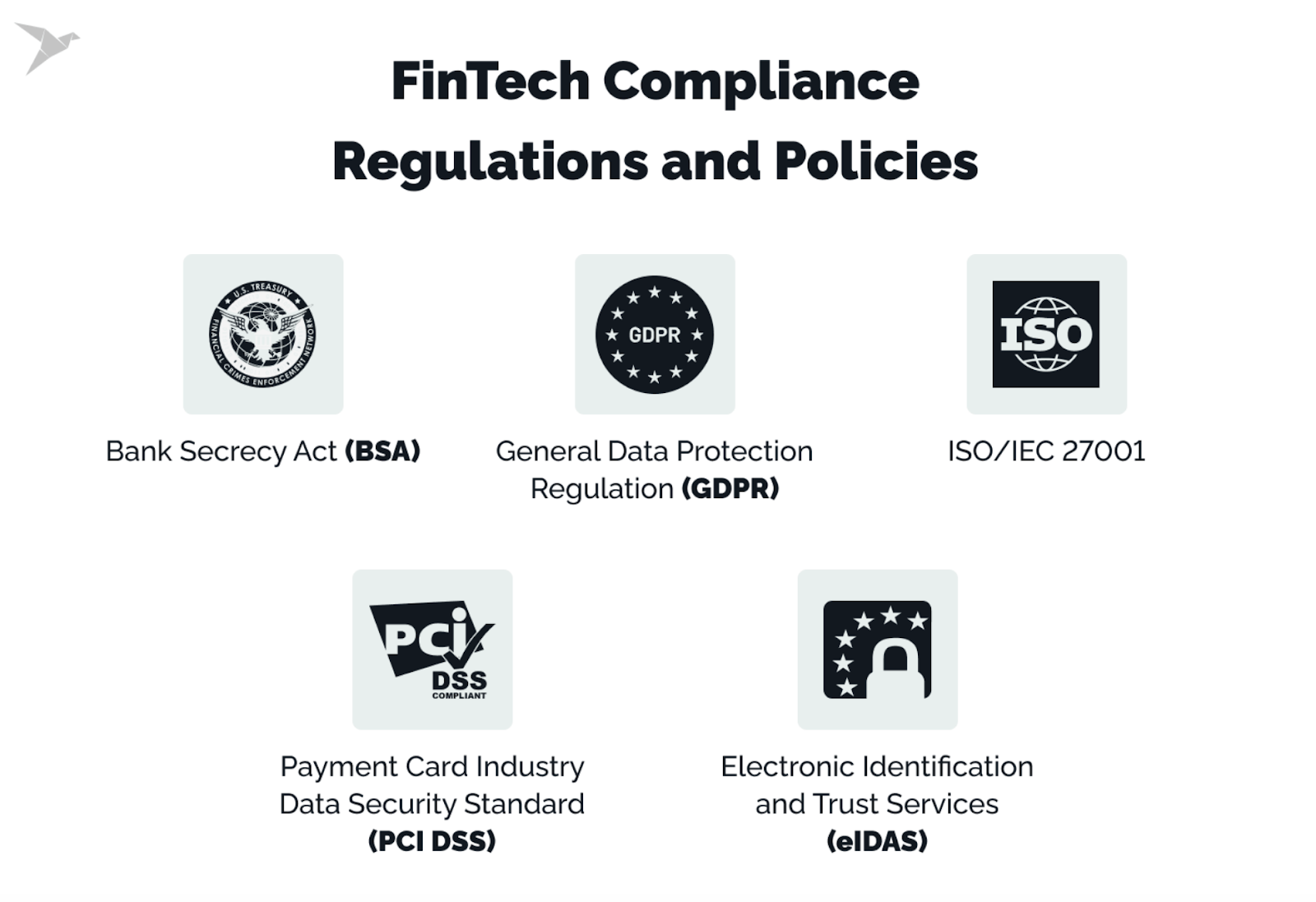

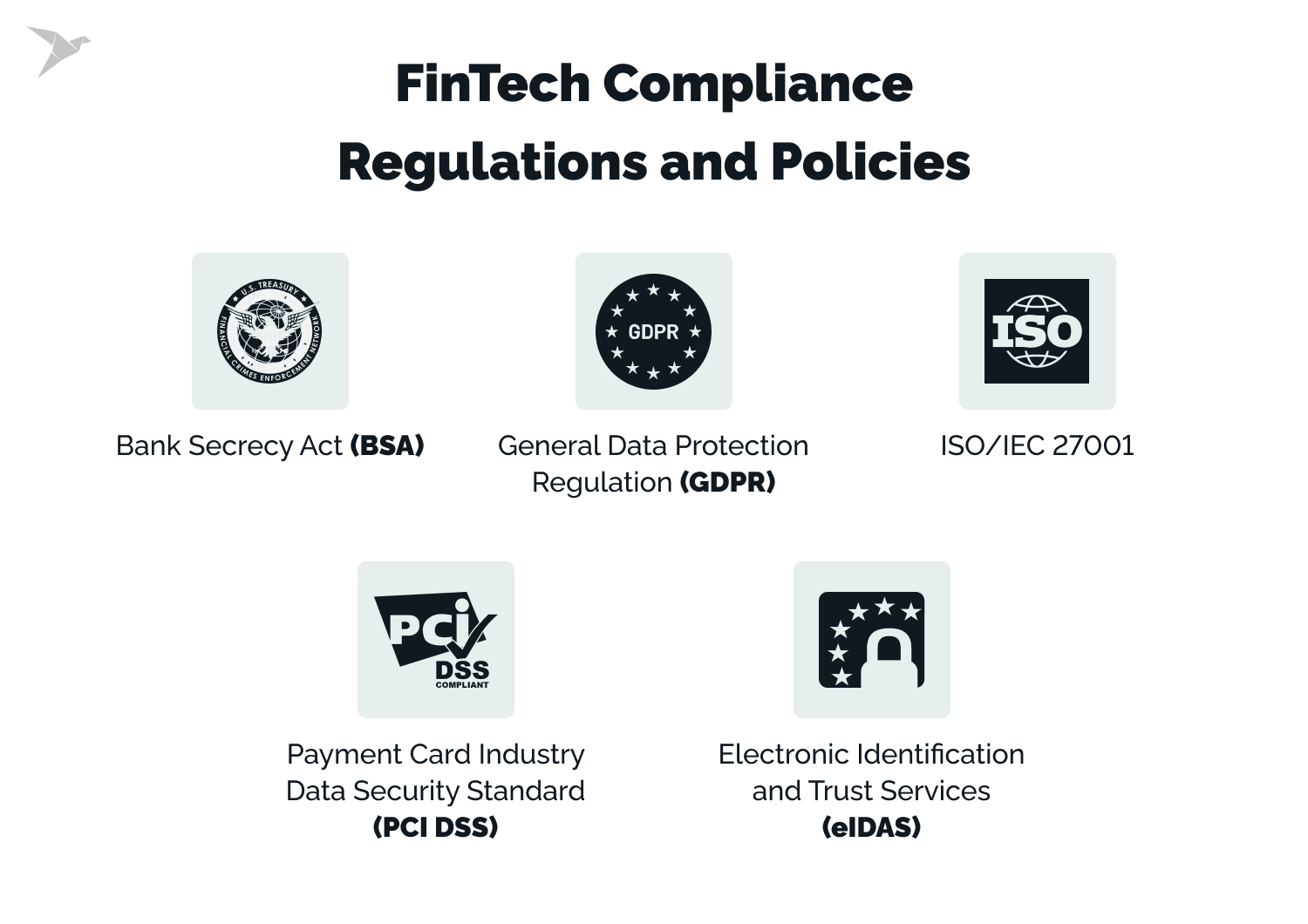

6. Complying with Evolving Regulations and Fintech Industry Standards

Source

Adherence and compliance: two notions every financial technology company must be quite familiar with by now. As we all know, the vast world of regulations poses one of the most significant fintech challenges.

As financial technology companies expand globally, they face complex compliance requirements that differ across regions. Key areas like:

- Anti-Money Laundering (AML)

- Payment Service Directive 3 (PSD3)

- Know Your Customer (KYC) and Know Your Business (KYB)

- Payment Card Industry Data Security Standard (PCI DSS)

…are just the tip of the iceberg. These regulations require constant updates and adherence, which, although costly and time-consuming, are non-negotiable.

In an industry where trust is paramount, especially when handling customers' financial data, adhering to all regulations is key. Failure to do so can lead to hefty fines, legal consequences, and serious damage to reputation.

As such, one significant fintech challenge is the need for continuous investment in regulatory technology (RegTech). This involves:

- The actual investment in RegTech tools and tech partners (essential for staying compliant in today’s regulatory environment)

- Ongoing process updates (constantly adapting and refining processes to meet new standards)

- Team training (so that employees are up-to-date with the latest compliance requirements)

For fintechs operating across multiple jurisdictions, the compliance burden intensifies. Each jurisdiction has its own set of rules, making compliance a continuous and evolving effort.

To stay competitive, fintechs must integrate compliance into their business models, and that’s a given. Fortunately, it’s not all bad news. Using advanced technologies like AI and machine learning to automate and improve processes is a major step forward, aiding this process greatly.

Adherence to evolving regulations doesn't have to be a burden — it can be a strategic advantage. Take the example of Token Financial Technologies. By partnering with Zitec, Token was able to launch a PCI DSS-compliant payment platform in less than nine months. Moreover, this financial technology project opened new doors for rapid expansion across Europe.

7. Aligning Digital Investments with Market Needs for Strategic Innovation

Source

With the rapid adoption of digital financial services and the increasing role of AI, blockchain, and machine learning, there is constant pressure to develop new products that meet evolving consumer needs.

For example, the surge in demand for personalized financial services has led companies like Apple and Klarna to launch innovative products, such as:

- Apple’s P2P payments via iPhone

- Klarna’s new credit card options.

Keep in mind that not all innovations lead to success. The fintech sector has seen many instances where large investments in new products did not yield the expected returns.

So, how can one determine which product developments will deliver the best ROI? Tough to say. One approach for fintech companies is to “fail fast”.

Companies can no longer afford to invest in every promising idea, especially without a clear path to profitability. Hence, fintechs are switching focus to areas with a competitive advantage or a clear market demand.

How can you navigate this fintech challenge?

- Collaborating with other fintech firms helps share the financial burden and tap into external expertise. While this approach accelerates time to market, it raises the potential issue of a shared competitive edge.

- Adopting a "fail fast" mindset can drive meaningful innovation. In practice, that translates to developing Proofs of Concept (PoCs) and Minimum Viable Products (MVPs) to quickly test and validate ideas, similar to what we did for the first Romanian blockchain-enabled neobank. This minimizes risks and reduces the time and cost associated with full-scale development.

Our fintech experts are here to help you define your strategic vision and get started with a PoC. Reach out today.

Face all your fintech challenges with a trusted digital transformation partner by your side

As we’ve explored, the fintech landscape is filled with both opportunities and challenges. From navigating regulatory complexities to balancing innovation with cost management, fintech companies must be agile and strategic. Embracing a fail-fast mentality, validating ideas through small-scale successes, and leveraging partnerships for rapid development are key strategies for staying ahead.

However, it's crucial to remain cautious and selective. Invest time and resources in areas that truly matter and align with long-term goals.

Face these fintech challenges head-on, starting today. Partner with Zitec — the go-to European digital transformation leader.

Don't Just Keep Up with the Future - Shape it.Reach out. Whenever You're Ready.

|

Share via:

{kind=link}